Supply chain management is an integral part of both the retail and food businesses. Think of it as the equivalent of the troves of databases that are required to run quant funds and HFT operations. Without their data, algorithms can’t be backtested, strategies can’t be run. Without efficient supply chain management, products can’t get to where they need to go, and suppliers have more trouble finding distributors. We haven’t even begun to discuss the potential inventory issues that can spring up if supply chain management isn’t up to snuff. Well, enter Park City Group (PCYG). The company operates in a $2B+ addressable market with a significant runway for future growth while achieving extraordinary economies of scale. The company sports a strong balance sheet with close to $15MM in cash and 12% Debt/Total Capital. Management’s interests are aligned with its shareholders as insiders own close to 33% of shares. Revenues are growing at a 23.4% 5 Yr CAGR, and a 70% FCF Yield 5 Year CAGR. At current trading levels, Mr. Market is offering shares with 40%+ upside potential.

Park City Group is a SaaS (Software-as-a-Service) company that develops, markets, and supports its proprietary software products. Their software provides advanced commerce and supply chain solutions that enables the retailer and supplier to manage inventory, product mix, and labor. The company also offers its software ReposiTrak, a cloud based compliance solution that helps food, pharmaceutical, and dietary supplement retailers and suppliers to protect their brands and remain in compliance with regulations. On top of compliance, ReposiTrak provides business consulting services to suppliers and retailers in the grocery, convenience, and speciality retail industries. In other words, ReposiTrak connects buyers with sellers. Here’s what’s interesting: Park City Group is the world’s only company with a sourcing, compliance management, and advanced commerce platform for retailing. To really understand the business and value proposition, we have to dig into the industry drivers, and where PCYG fits.

Business Overview

Market Changes

In their latest company presentation, PCYG highlighted three major market trends it’s seeing in the $2B Food retailing industry; Changing Consumer Demands, New Competitive Threats, and Increased Regulatory Risk.

Consumer demands are changing rapidly in the food retail business. More people are switching from big-brand retailers to more local (dare I say) organic products. In general, consumers are getting more specific. This specificity is creating complex, difficult to source supply chain problems. Moving on to competitive threats; Amazon is disrupting the industry (there’s a surprise). Amazon’s purchase of Whole Foods shines light into the need for the food industry to accelerate adoption of newer technology, especially when it comes to product sourcing. Finally, The Food Safety Modernization revamped their food safety regulations by putting responsibility on food retailers for the safety of their supply chain. This new regulation drastically increases the risk for new liabilities.

All of these changes in industry put PCYG in an excellent position to capture market share. Now that we’ve got an idea on what is going to drive the industry heading into the future, let’s see how PCYG operates to address the needs of each segment of change.

Brief Overview of ReposiTrak

The company offers three main solutions under its software products: Compliance, Supply Chain, and B2B e-commerce. By breaking each solution down, it’s easier to see the value proposition and the potential appreciation of share price.

To solve each issue, PCYG offers ReposiTrak. ReposiTrak is the industry standard for food safety and consumer product compliance. Moreover, ReposiTrak landed endorsements from the Food Marketing Institute, Retailer Owned Food Distributors & Associates, and the Global Market Development Center. These are big institutions that all claim ReposiTrak as their “one stop shop” for all things compliance. ReposiTrak helps food retailers and food service operators ensure compliance with various regulations, while protecting their brands and reducing risk of food bourn illnesses and product recalls. ReposiTrak’s success eventually led it to another sponsorship from the Safe Quality Food Institute, which awarded ReposiTrak to host the industry’s largest audit schema.

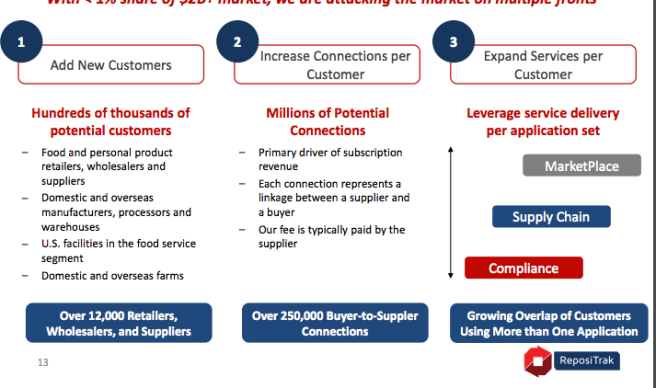

ReposiTrak is the most valuable part of the entire business, so its important to understand how it generates revenues for the company. ReposiTrak runs a “Hub and Spoke” business model. The “hubs” are the retailers and wholesalers, and the “spokes” are the suppliers of the retailers and wholesalers. This means that once ReposiTrak is used on the retail / wholesale end prompts the suppliers of those stores to sign up for the service to become compliant. The company charges a low monthly fee for the ReposiTrak service. This fee builds up, remember, due to the millions of potential connections between retail/wholesale and the supply side in the food and consumer product supplier chain. PCYG’s management is projecting a $2 Billion + addressable market for this very solution alone.

Current Industry Challenges with Supply Chains

There are three main challenges facing most companies in PCYG’s targeted industry’s supply chain management: 1) Enhanced Supplier Sourcing, 2) Stronger Supplier Vetting, and 3) More Efficient Transacting. The first supply chain issue goes hand-in-hand with the overall trend of the industry in that more and more consumers are demanding locally sourced products. This creates a need for retailers to efficiently source from the best local vendors while displaying a wide array of products.

Stronger supplier vetting is another major issue because as supply chains become more complex, it increases the overall risk of the retailer to stay in compliance with their supply chain regulations, especially in the food consumer business.

Finally (and most importantly), the consumer product retailing industry isn’t the best business to be in if you’re looking for high margins and low turnover. Historically product retailing businesses sport low margins and high turnovers. Due to the low margin nature of the industry, companies should look to be cutting costs wherever they can to gain that marginal advantage over competitors. ReposiTrak is the solution to companies that want to reduce their working capital and funnel that cash back into the business, increasing ROI in the process.

Why ReposiTrak is The Solution To Supply Chain Issues

Being the solution helps when you’re the only single source one-stop-shop solution to all three of the above challenges. ReposiTrak accomplishes this by sourcing, vetting, and transacting all under the same roof, so to speak (which we discussed earlier). The company already possesses impressive businesses of scale, servicing over 250,000 supplier/buyer connections, with potential to grow into the millions. The growth will be triggered by the need of suppliers and retailers to respond to Amazon’s fully connected network of suppliers. If retailers want to compete, they’re going to need to adapt, ReposiTrak is part of that adaptation process. Finally, ReposiTrak’s business model is effectively self-reinforcing. The network effect they generate with increased supplier/retailer connections drives the growth of its product, while at the same time enhancing the value of all the other services it offers.

Explanation on Network Effect & Self-Reinforcing Model

To fully understand the moaty-ness of PCYG, it’s important to spend a bit more time discussing the three-part solution of ReposiTrak, and how each part enhances the value of the other. The sourcing solution, MarketPlace, provides retailers and wholesalers an easy and efficient way to find, connect, and transact with vendors. Through the MarketPlace, retailers / wholesalers can sample products, receive private digital catalogs, and enjoy turnkey services such as concierge, EZ vendors, and automated on-boarding for new vendors. This part of the business model is what gets PCYG’s foot in the door.

According to the company, the Compliance side of the business is what drives the scale of their network effect. This can be seen through their various industry endorsements. It also doesn’t hurt that this part of their business is driven by the necessity of retailers/wholesalers to stay in compliance or face legal consequences. In other words, this makes ReposiTrak’s connection potential infinite in the US Food and Consumer Product supply chain space.

The final part of this three-step process is the actual Supply Chain management side of the software. The company touts that their supply chain management software increases the scope of their customer engagement. ReposiTrak’s supply chain helps customers reduce the cost of exchanging data, improves accuracy, and lowers inventory levels while increasing sales. The self-reinforcing comes when customers then leverage the ReposiTrak MarketPlace network to increase PCYG’s revenue per connection (think snowball effect). This chart from the company’s latest investor presentation wraps up their business model perfectly.

Future Growth & Number Crunching

Many Avenues for Potential Growth

PCYG is optimistic about both the future growth of revenues and profit on an annual basis. On the revenue side, the growth could come from the large market PCYG operates in, with the potential to serve upwards of 1 million customers. Secondly, new regulatory threats (read: The Food Safety Modernization Act), Amazon’s purchase of Whole Foods, and a demand for increased product differentiation could drive revenues higher. Finally, ReposiTrak’s self-reinforcing B2B business model has a logical migration from each app to the next.

On the profit side of things, the company is already at an advantage by being an SaaS. The company has a scalable technology platform and is actively seeking to increase automation within their operations. This trickles down into high incremental margins. Finally, the company has long-standing relationships with its customers. Don’t take my word for it: ReposiTrak has a >90% retention rate, and it’s always more cost-effective to keep a customer than to acquire a new one.

Diving Into Financials

Revenues grew 35% from 2016 – 2017, and since 2013 have grown at a 13.7% CAGR clip. Net income from 2016 – 2017 grew from $0.7M to $3.8M, an increase of 467%, that’s some serious operating leverage off of revenues.

The company earns 71% gross margins, 23% EBITDA margins, and 20% net income margins. With $14M in cash on the balance sheet, the company has enough liquid cash to pay off all of its total liabilities. Over the last year, the company generated $1.2M in FCF compared to a loss of $500K the year before. Last year revenues topped out at $19M with $4M in Operating Income.

Finding A Fair Value

PCYG won’t pass a standard “value” screener, which is something I’m starting to learn more and more of: Great businesses at ridiculous prices don’t always screen well! On the surface you’re looking at a company that’s trading at nearly 70x earnings and 10x book value (I can feel Ben Graham roll in his grave). Looking deeper you find that PCYG is trading at only 27x earnings, and its EV/Revenues is only 5.4x.

Analysts are currently projecting revenues to be $22M, $28M, and $35M over the next three years. That’s revenue growth of 17%, 28.5%, and 23% respectively (doesn’t seem out of reach given the 5 year average). If we average 19% and 22% growth for the last two years, we end up with $42M in revenues by 2022. From this $42M in revenues the company would see $19M in EBIDTA. Earnings are being projected at $0.19, $0.26, and $0.40, which would bring PCYG’s P/E from 68 to 20x by 2021.

Looking at CapEx, the company spends on average 4.5% of revenues. This is a bit misleading because the company spent next to nothing ($500K) every other year before spending $2M over the last year. For this reason I’ve assumed at least $1M in CapEx every other year, with $2M in CapEx in between. This is to account for any new business that the company might generate which would force some expansion and increased CapEx.

From here we can get an idea of FCF by subtracting taxes (assuming a 23% tax rate) to get NOPAT of $12MM by 2022. From here we subtract out our CapEx and add any D&A to arrive at $14MM in FCF.

Now we can get an idea of our range of Enterprise Value. Adding up all the years future cash flows we get a PV of Discrete Cash flows at $27MM. Assuming a perpetuity growth rate range of 3.50 – 4.50% we get roughly $14MM in terminal FCF (the number we arrived at earlier). Taking our terminal discount factor range of 68% – 71% we can a PV of terminal value between $149M – $225M. Adding both PV’s gets us an Enterprise Value range of $176M – $253M.

From our EV, we add back in cash & investments and subtract any debt on the balance sheet. This gives us a Common Equity Value range of $187M – $264M. Dividing that range by shares outstanding gives us a fair value range of $9.47 – $13.36 per share. This fair value range would mean an implied revenue multiple of 4.2x – 6.2x, which isn’t out of the realm of plausibility given the 5.4x EV/Revenues the company currently does.

Reading The Tape

I started a 100bps position a few days ago after price rebounded off support levels at the $7 price. I did something different this time in that I didn’t put any stop losses. Instead, I risked 100bps by buying 100 shares of the company for $8,000 (averages out to 1% of total capital). With higher conviction investments, I am starting to play around with not using stops and setting just a share limit to get to my ideal risk target.

Where Is My Fallibility?

From an accounting perspective, PCYG is extremely durable. The biggest threat to my bullish thesis will come in a reduction of growth in the number of customers they acquire. Since the company operates on a Hub and Spoke Model, a steady generation of customers will ensure very successful growth in the future. However, this isn’t too much of a worry because the company can already utilize its 250,000 connections, develop deeper relationships, and continue to add services to its existing customers.

Secondly, if regulations begin to loosen in the US Food Industry, you could see more rationalization from retailers and wholesalers not to pay for ReposiTrak services due to the fact that with relaxed regulations they won’t get hit as hard.

Although ReposiTrak is the only single source solution currently available, this is the technology sector we are talking about. There is always a chance that a competitor comes in with a faster, more efficient way of streamlining supply chain, market place, and vetting. Yet as I typed that I realized that the switching costs of changing a system like ReposiTrak might be astronomical for retailers / wholesalers given the dense network that’s been established.

Please comment below if I am missing any red flags that would put a serious damper on the bullish thesis I’ve laid out.

https://www.dropbox.com/s/q27aa6y8dxn49hf/Park%20City%20Group%20An%20Imaginary%20Growth%20Story%20With%2065%25%20Downside%20-%20Park%20City%20Group%2C%20.pdf?dl=0

LikeLiked by 1 person

Joe,

Thank you for shining light to the bearish side of the investment. The analysis was both detailed and thoughtful. I will dig into this more and see if it changes my valuation of the company / business going forward (analysis was done in 2014, which makes me wonder how applicable it still is).

Nevertheless I greatly appreciate you dropping a comment.

Thanks for reading.

Brandon

LikeLike

Good article. Thanks for sharing.

LikeLike

Thank you for reading!

LikeLike